What the 2025/26 Customs Tariff Book Covers

The official Customs Tariff 2025/2026 is Nepal’s master list of import and export duty rates, based on the Harmonized System (HS 2022, 7th Edition). It contains:

- General rules for interpreting HS codes (how to classify any product).

- Schedule 1 & 2: Import customs duty rates for each HS code.

- Schedule 3: Export customs duty rates where applicable.

Every importer, exporter, and customs broker is supposed to use this book plus the annual Finance Act amendments when calculating duties.

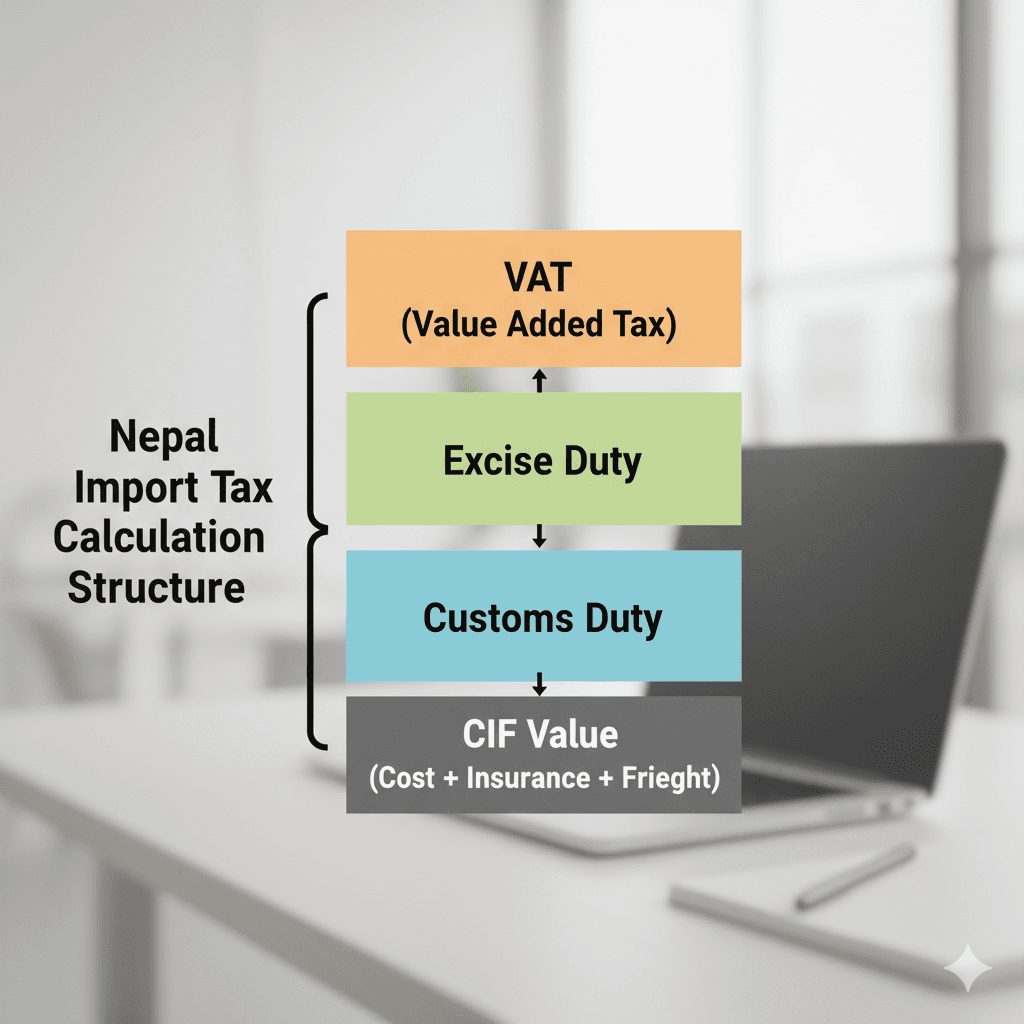

How Nepal Calculates Import Taxes in 2025/26

The tariff book gives you the basic customs duty rate, but your final landed cost also includes other taxes.

- Find HS Code – Classify goods using HS 2022 (e.g., 5201 for cotton, 8517 for phones, 8703 for cars).

- Determine Customs Value (CIF) – Cost + Insurance + Freight to Nepal border/airport.

- Apply Customs Duty –

Customs Duty = CIF × duty %from the tariff book. - Add Excise (if applicable) – Often on alcohol, tobacco, vehicles, some luxury items.

- Apply 13% VAT – On CIF + customs duty + excise.

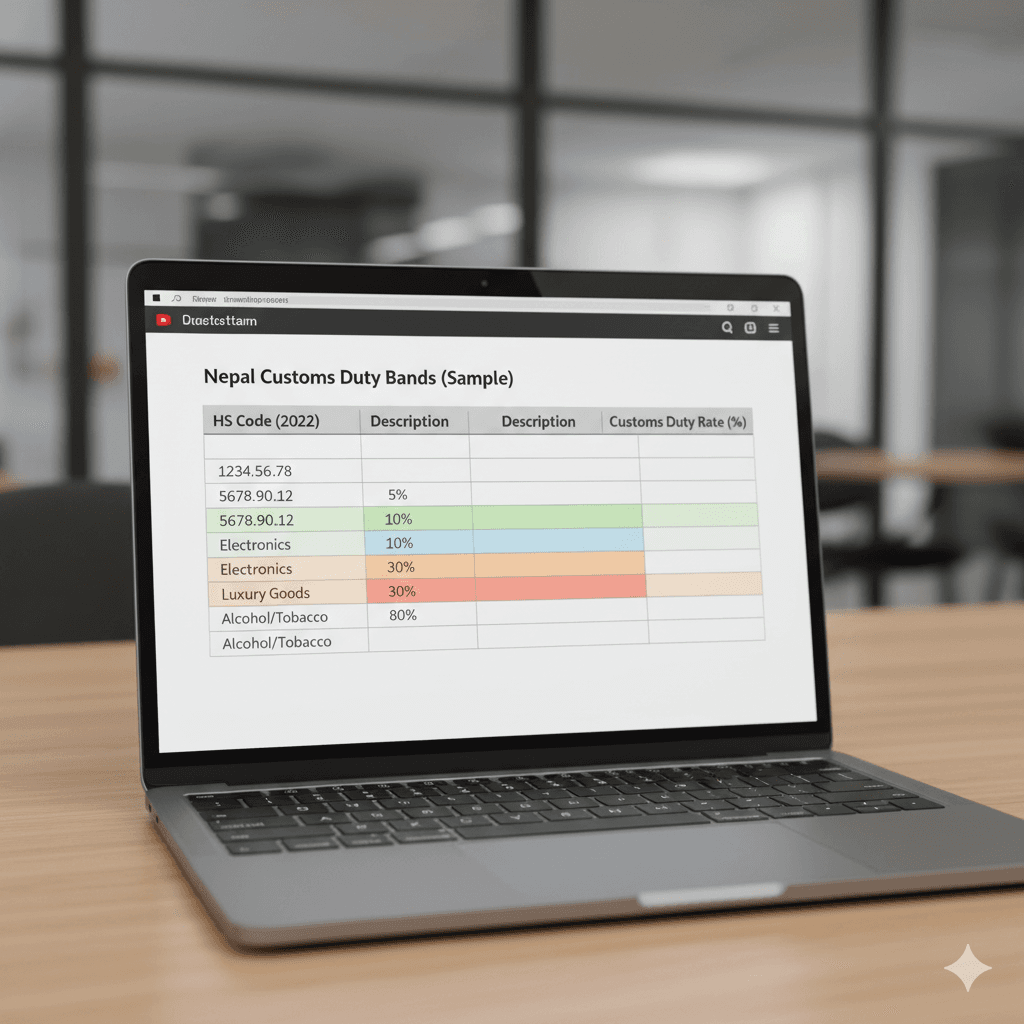

Typical duty bands run from 0% to 80%, with lower rates for essentials and raw materials, and higher for luxury/consumer items.

Key Tariff Bands by Product Category

From the 2025/26 tariff and tax guides, most goods fall into broad

- Raw materials & machinery

- Cotton (HS 5201) and industrial inputs: 5–10% duty, 0% excise, 13% VAT.

- Production machinery: often 5% or lower; some green/agro machinery at 1% or 0% under new incentives.

- Everyday consumer goods

- Processed foods, snacks, mid‑range electronics: 10–30% duty, 13% VAT; some face small or no excise.

- Vehicles

- Passenger cars (HS 8703): around 40–240% effective duty depending on engine size, type, and age, plus excise; then 13% VAT.

- Sin goods (alcohol, tobacco)

- Beer (HS 2203) and liquor: 30–100%+ customs duty, high specific excise per litre, 13% VAT.

- Cigarettes: very high specific excise (e.g., Rs 4,500 per 1,000 pieces) on top of duty.

Recent Finance Bill 2082/83 (2025/26) tweaks include:

- Higher duties on alcohol, beer, tobacco, and cigarettes.

- Removal or deep cut in duty (often to 1%) plus exemption of other taxes for machinery for organic fertilizer and some hydropower‑related imports.

Policy Direction: Protecting Local Industry, Encouraging Priority Sectors

The 2025/26 tariff schedule and Finance Bill show a clear strategy:

- Protect local manufacturing and health

- Higher tariffs on processed snacks, luxury goods, and harmful products (alcohol, tobacco).

- Support production & agriculture

- Minimal or 1% customs duty and tax exemptions for machinery used in organic and natural fertilizer production and some agri/energy projects.

- Hydropower & infrastructure push

- Special 1% customs duty regime with VAT exemptions for approved hydropower projects on key equipment, released via bank guarantee.

- Simplification for traders

- Removal of the NPR 300,000 EXIM code bank guarantee for import/export businesses to ease entry into trade.

For importers, this means: higher landed costs on non‑essential consumer goods, but lower barriers for productive, export‑oriented, or green sectors.

Practical Example: Calculating Duty on an Imported Machine

- CIF value of weaving machine: USD 10,000.

- Basic customs duty rate (from tariff): 5%.

- Excise: 0% (industrial machine).

- VAT: 13%.

- Customs duty = 10,000 × 5% = 500.

- Taxable base for VAT = 10,000 + 500 = 10,500.

- VAT = 10,500 × 13% = 1,365.

Total tax = 500 + 1,365 = 1,865 → effective tax rate ≈ 18.65%, not just “5% duty.”

Where to Check Exact Rates for Your HS Code

For each product, you should:

- Confirm the correct HS code (using the HS 2022 structure).

- Look up the import duty % in the tariff book.

- Check Finance Bill notes for temporary increases/reductions or exemptions.

- Apply VAT and excise rules as per your category.

Working with a customs broker or freight forwarder (like Sea Sky Cargo) helps avoid misclassification, penalties, or overpayment.