Introduction

A cargo insurance claim becomes important the moment a shipment is lost, damaged, or delivered in a condition that does not match what was booked. For importers and exporters, the best time to understand the claim process is before anything goes wrong, because fast reporting and clean documentation make a major difference in how a claim is handled.

Freight insurance is designed to protect goods during transit, but it does not work like a simple refund button. To recover money successfully, the shipper usually needs evidence, timing, and complete documents that prove what happened and what the loss is worth.

What cargo insurance covers

Cargo insurance is meant to protect shipments against risks such as theft, damage, and total loss during transport. Depending on the policy type, coverage may apply to sea freight, air freight, road freight, or multimodal shipments.

Many businesses assume carrier liability is enough, but that is not always true. Carrier limits can be far lower than the real value of the cargo, which is why freight insurance is often used as a separate layer of protection.

Why claims happen

Claims usually happen after incidents such as container damage, wet cargo, missing cartons, rough handling, theft, fire, or delivery shortages. In some cases, the cargo arrives, but the packaging or contents are damaged enough that a claim is still necessary.

The biggest mistake is waiting too long to act. Once the cargo is accepted without proper notes, or once evidence is lost, the claim becomes harder to prove and may even be denied.

First steps after damage

The first priority is to protect the shipment and preserve the evidence. If the damage is visible at delivery, the consignee should note it on the delivery receipt or transport document before signing clean acceptance.

The next step is to take photos and videos of the cargo, packaging, seal, and overall condition of the container or pallet. The damaged goods should be kept in the same condition until the insurer or surveyor inspects them, because altering them too early can weaken the claim.

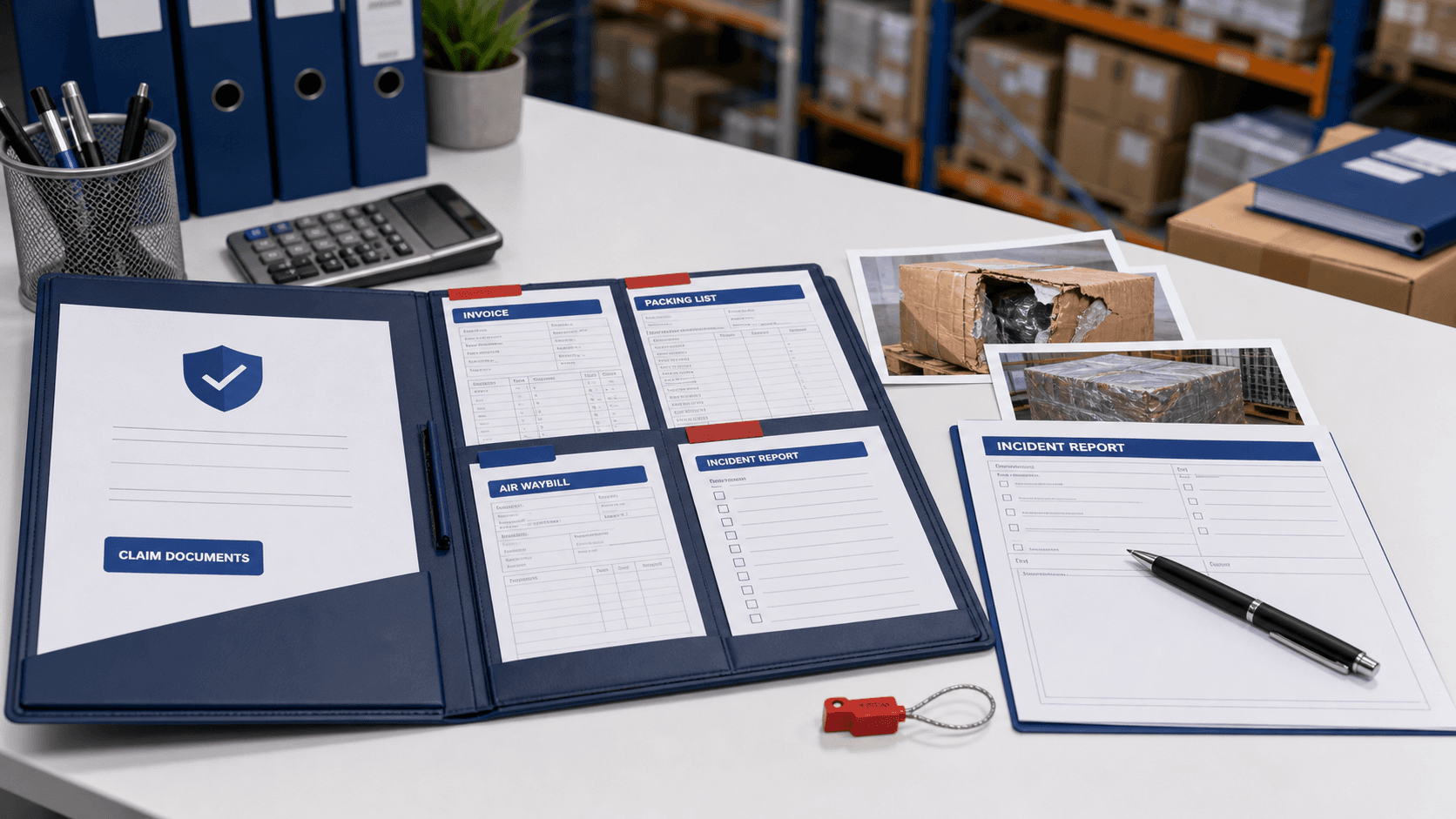

Important documents

A cargo insurance claim is usually supported by several core documents. These often include the commercial invoice, packing list, bill of lading or airway bill, insurance policy or certificate, photos of the damage, and a written statement describing the incident.

Depending on the case, the insurer may also ask for a claim form, survey report, repair estimate, salvage value, delivery receipt with exceptions, or a non-receipt statement if the shipment is missing. The more complete the file, the easier it is for the insurer to assess the loss.

Recommended

Cargo insurance claims are easiest to win when the shipper acts quickly, preserves evidence, and keeps the paperwork complete. For importers and exporters, freight insurance is not just a backup plan; it is a practical way to protect cargo value during international shipping. If your business moves goods regularly, the smartest approach is to combine good packaging, accurate documents, the right freight insurance, and a logistics partner that understands risk. Contact SeaSky for a quote or consultation if you want help with freight planning, customs support, and shipment protection.

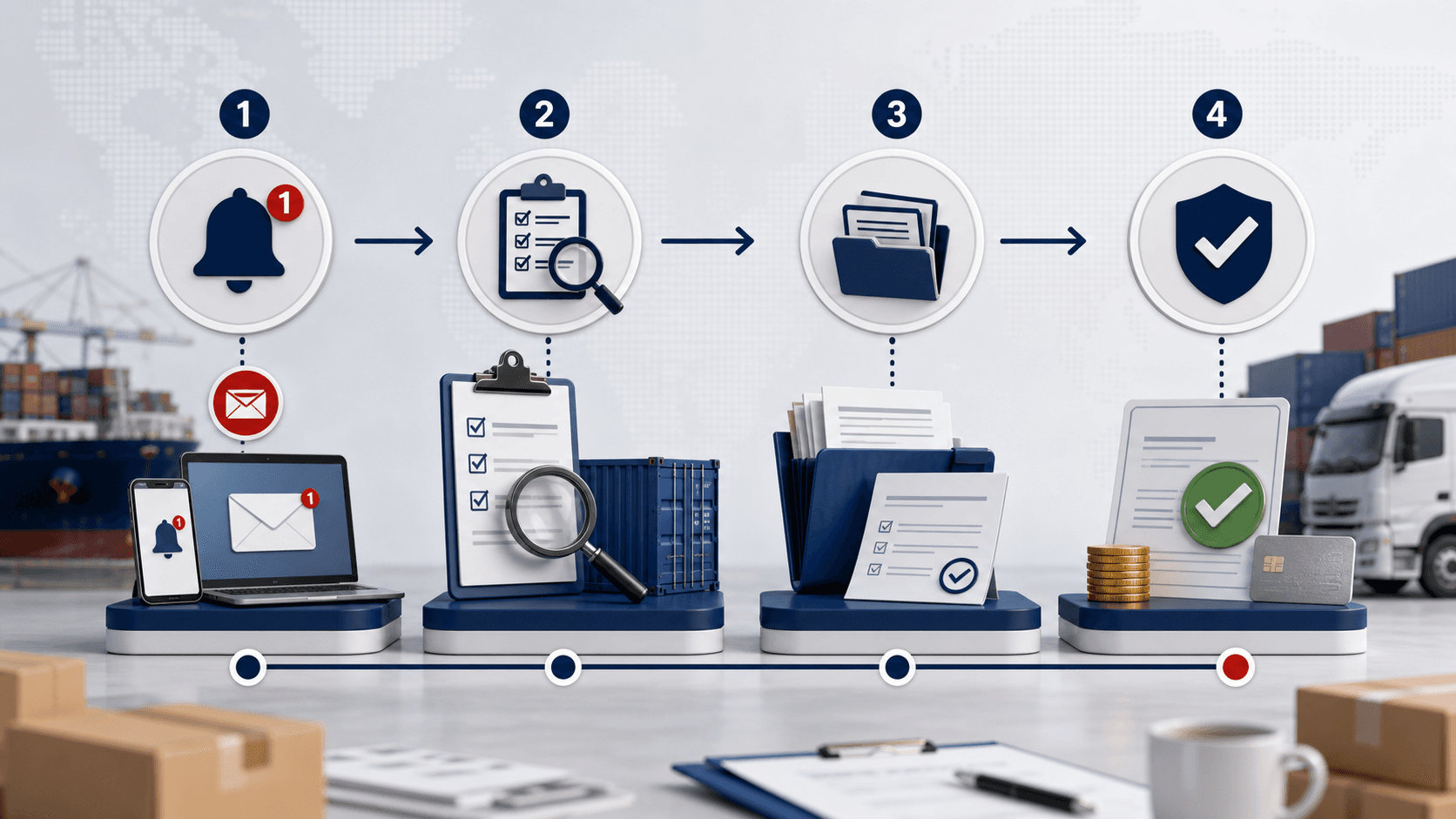

How the claim process works

The claim process usually starts with immediate notice to the carrier and the insurer. After that, the insurer may request more documents, a survey, or a written explanation of how and when the damage occurred.

Once the claim file is complete, the insurer reviews the evidence and decides whether the loss falls under the policy terms. If approved, payment is based on the insured value, the type of damage, and the conditions of the policy.

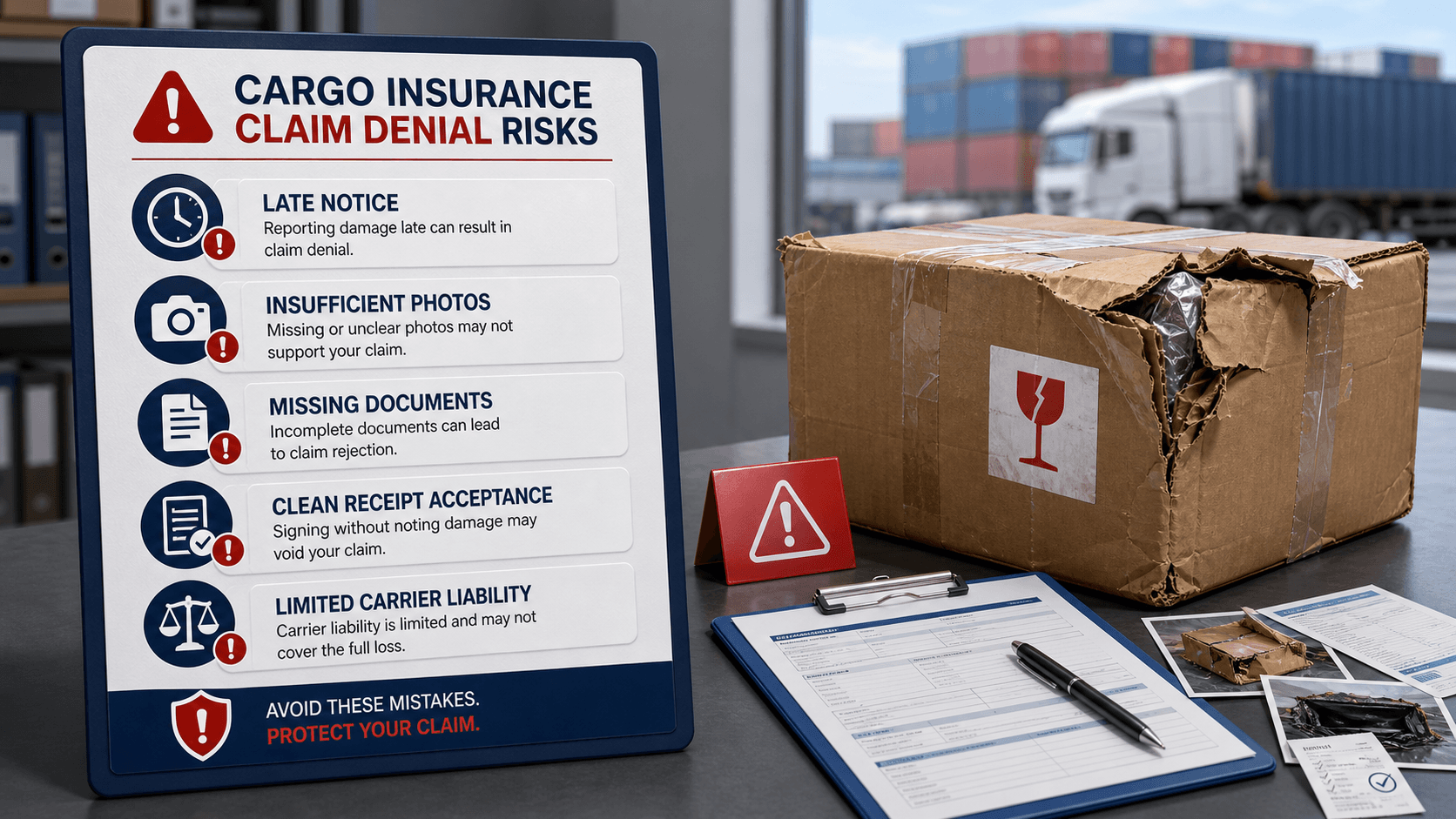

Common reasons claims are denied

Claims are often denied or reduced because the shipper did not report the damage on time, gave a clean receipt, failed to keep the damaged goods, or submitted incomplete evidence. Missing photos, missing transport documents, and vague loss descriptions can also create problems.

Another common issue is confusing freight insurance with carrier liability. If the cargo is only covered by carrier responsibility and not a proper freight insurance policy, the payout may be limited even when the loss is real.

How to protect future shipments

The best protection starts before shipping. Importers and exporters should use strong packaging, confirm cargo value correctly, choose the right insurance coverage, and keep shipment records organized from the beginning.

It also helps to inspect the shipment at handover, note any damage immediately, and train staff not to sign a clean receipt if there is visible loss or damage. These simple habits can make the difference between a successful claim and a denied one.

How Sea Sky Cargo helps

Sea Sky Cargo supports shippers with customs coordination, freight planning, and shipment handling, which helps reduce the types of problems that often lead to claims. While insurance is a separate product, good logistics support can reduce risk by improving routing, packaging guidance, documentation, and cargo control.

For importers and exporters, this matters because fewer handling mistakes usually mean fewer damage issues and fewer disputes later. A strong freight forwarding partner cannot prevent every incident, but it can make the shipment more resilient and the claims process easier to manage if something does go wrong.

Conclusion

Cargo insurance claims are easiest to win when the shipper acts quickly, preserves evidence, and keeps the paperwork complete. For importers and exporters, freight insurance is not just a backup plan; it is a practical way to protect cargo value during international shipping.

If your business moves goods regularly, the smartest approach is to combine good packaging, accurate documents, the right freight insurance, and a logistics partner that understands risk. Contact SeaSky for a quote or consultation if you want help with freight planning, customs support, and shipment protection.

Get Quotes

Share your shipment details and our team will send a practical quote with the right mode, timing, and cost path.